Their business started out years ago providing a mail-back service for unused medication and, over time, grew into providing onsite containers in medical offices and pharmacies. Another revenue stream is their route-based business of onsite medical-waste collection.

Their business started out years ago providing a mail-back service for unused medication and, over time, grew into providing onsite containers in medical offices and pharmacies. Another revenue stream is their route-based business of onsite medical-waste collection.

Let’s be honest – it’s really a BORING company – something you wouldn’t brag about owning on the golf course.

ClearPoint Neuro is based in California and is a medical device company that has developed a platform for performing minimally invasive surgical procedures in the brain.

What makes ClearPoint so unique from other competitors: their ClearPoint system is the only surgical platform that provides real-time MRI guidance for a range of minimally invasive procedures in the brain. This ultimately provides a never-before surgical option for patients with neurological disorders such as Epilepsy, Parkinson’s and ALS, among others.

Although still in its infancy, ClearPoint’s technology has a multitude of other applications, including treatments for gene therapy and drug delivery, expanding its total addressable market.

What makes Intellia Therapeutics so unique from other biotech companies: they use CRISPR technology that enables alteration of DNA and the modification of gene function, which ultimately can cure many diseases and conditions such as Leukemia.

Some experts predict that the CRISPR technology is so powerful – to the point where genetic disorders may become a thing of the past.

IES is based in Houston and is a holding company for industrial products and infrastructure services.

They started out as a group of electrical contractors years ago, but in the last decade they have diversified by acquiring different business lines…very similar to a roll-up.

They now have four different business lines: Communications, Residential, Infrastructure Solutions, and Commercial and Industrial. Residential is by far the fastest growing.

Let’s be honest – it’s really a boring company. But when you look under the hood…

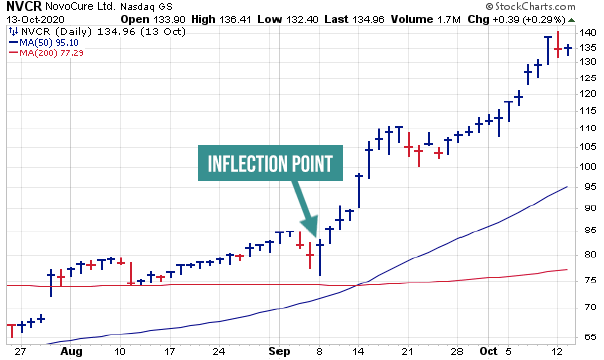

Novocure is a medical products company developing novel therapy treatments for cancerous tumors including brain cancer.

What makes Novocure so unique: they use electric fields tuned to specific frequencies to disrupt cell division, which ultimately inhibits tumor growth and potentially causes cancerous cells to die.

Founded in 1951, Kulicke & Soffa is a Pennsylvania-based semi-conductor manufacturer specializing in back-end electronic assembly solutions for automotive, consumer, communications, computing, and industrial markets.

Founded in 1951, Kulicke & Soffa is a Pennsylvania-based semi-conductor manufacturer specializing in back-end electronic assembly solutions for automotive, consumer, communications, computing, and industrial markets.

Key underlying growth drivers for KLIC include Smartphone, Internet-of-Things (IoT), 5G, LED Lighting, and cloud computing.